Third-party payment was originally used as a credit intermediary to solve the trust problem of buyers and sellers in e-commerce. Alipay is the earliest third-party payment institution in China. After decades of development and financial innovation, many third-party payments, including Alipay, Tenpay, Lakara, and fast money, have become an indispensable part of e-commerce and Internet finance. This paper analyzes the business model and tax treatment of third-party payment in accordance with the “Administrative Measures for Payment Services of Non-financial Institutionsâ€, “Administrative Measures for Network Payment Services of Non-Bank Payment Institutions†and relevant tax laws.

I. Overview of third-party payment services

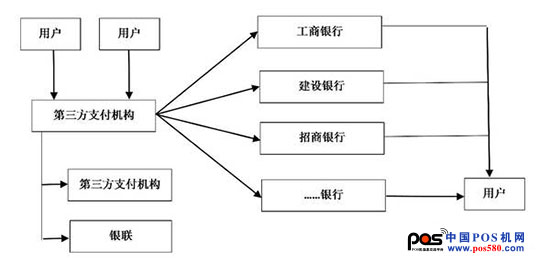

The third-party payment institution belongs to a non-bank financial institution, and the People's Bank of China approves and issues the Payment Business License. The payment service provided by the third-party payment institution refers to the following part or all of the money transfer services provided as an intermediary between the payers: online payment, issuance and acceptance of prepaid cards, bank card receipts, and the determination of the People's Bank of China. Other payment services. The structure of the third-party payment service is as follows:

Description:

1. The user opens a third-party payment account and allocates funds as needed. Third-party payment institutions fully disclose the risks of network payment and maintain user rights.

2. The third-party payment institution signs cooperation agreements with the banks such as the “Billing Service Agreement†or the “Information Technology Service Agreementâ€, and transfers the funds to the other party through their account number in each bank according to the customer's instructions. Through third-party payment institutions, users can pay and refund all kinds of money conveniently, quickly and at low cost.

3. Due to the limited scope of the third-party payment institution's own business, it is impossible to sign a cooperation agreement with all banks. For unsigned banks, third-party payment institutions generally sign cooperation agreements (channel sharing) with UnionPay or other third-party payment institutions, and strive to fully cover the payment channels.

Second, the tax treatment of third-party payment business

(1) Settlement business

The settlement business is generally the main source of income of the third-party payment company, that is, the handling fee, or service fee, collected by the third-party payment institution when the user transfers funds through the third-party payment institution. At first, the third-party payment platforms, including Alipay, were exempt from fees for personal (2C) business, only for enterprises (2B), and the charging rate was extremely low, and the profit was generated by the huge amount of funds settled. At present, third-party payment companies represented by WeChat have begun to charge fees for personal business.

The cost of settlement business mainly includes the following aspects:

1. Settlement fee and information technology service fee paid to the bank. Since the third-party payment institution ultimately relies on the banks to make funds, it is necessary to pay the corresponding service fee of the bank when the funds are settled.

2. Human resources fees. The labor cost is the main cost of the third-party payment institution. Since the profit comes from the market share, it is necessary to continuously develop various systems, channels and models.

3. Equipment fee. For offline business, terminal equipment such as POS machines are generally installed. Since third-party payment agencies arrange thousands of merchants, the equipment is heavily invested.

Tax treatment:

For the settlement business income, according to the "Notice of the Ministry of Finance and the State Administration of Taxation on the comprehensive introduction of the pilot reform of the business tax to change the value-added tax" (Cai Shui [2016] No. 36), the value-added tax shall be paid in accordance with the "direct fee financial service". The tax rate is 6%. Direct-to-charge financial services refer to business activities that provide related services for money finance and other financial services and charge fees. Including providing currency exchange, account management, e-banking, credit card, letter of credit, financial guarantee, asset management, trust management, fund management, financial trading venue (platform) management, fund settlement, fund clearing, financial payment and other services.

(2) Provision for interest income

The deposit funds that have not been transferred out of the user account are also called reserve funds. The funds are not owned by the payment institution. The third-party payment institution should open a special deposit account for deposits in the commercial bank and store it. The statutory health interest shall be paid, and the use of the customer's reserve fund stored in the institution shall be supervised, and submitted to the legal person institution of the branch of the People's Bank of China and the depositary deposit bank where the deposit bank is located. Information such as the deposit or use of customer allowances.

Tax treatment:

Regarding the value-added tax involved in the interest income generated by the reserve fund stored in the special account, the third-party payment institution is not the owner of the reserve fund. In practice, the bank pays interest to the individual account, and the third-party payment then deducts the service from the personal account. fee. Among them, the interest paid by the bank to the individual belongs to the interest income of the deposit exempt from the value-added tax and personal income tax; the service fee deducted from the personal account by the third party payment, and the extra-cost charged as the settlement service income shall be in accordance with the “direct direct financingâ€. Service" pays VAT.

(3) Marketing expenses

In order to cultivate user spending habits, third-party payment agencies often cooperate with merchants to stipulate that consumers who use third-party payment platforms can enjoy certain discounts, and the discount amount is supplemented by third-party payment institutions to merchants.

Tax treatment:

For merchants, only the amount charged to the consumer should be subject to VAT, and the amount paid by the merchant to the third party should be understood as the income earned by the merchant for the marketing services provided by the third party, and the merchant should Pay a special invoice for marketing promotion fee VAT and pay VAT.

For individuals, according to the "Notice of the Ministry of Finance and the State Administration of Taxation on the Individual Income Tax Issues Related to Gifts for Promotion of Exhibitions in Enterprises" (Cai Shui [2011] No. 50), enterprises are required to sell goods to individuals through price discounts and discounts ( Product) and the price discount or discount obtained by providing the service are not subject to personal income tax.

(4) Derivative business

Agency business

With the innovation of Internet finance, third-party payment platforms have developed into online sales channels for financial wealth management products, such as the balance treasure products of Alipay platform.

Tax treatment:

The income from sales of wealth management products received by third-party payment institutions shall be subject to VAT in accordance with the “broker agency†service, and the applicable tax rate is 6%.

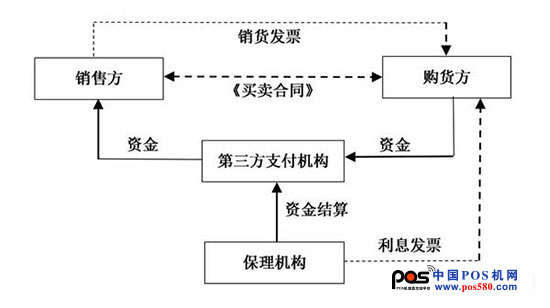

2. Factoring business

The third-party payment institution or its shareholders provide the installment payment service to the e-commerce platform buyers through the commercial factoring company, and the third-party payment company is responsible for settlement of the accounts. The business process is: After the buyer and the seller sign the "sales contract", the factoring company pays the purchase price to the seller who has the capital demand, and then sells the goods to the buyer, and the buyer pays the interest to the factoring company according to the agreed time limit. The factoring company and the buyer collect and pay through a third-party payment institution. Business process diagram:

Tax treatment:

Refer to Article 4 of the State Administration of Taxation on the Issues Concerning Value-Added Tax on the Period of the VAT Reform of Business Taxes (State Administration of Taxation Announcement No. 90 of 2015) Article 4 “Taxpayers providing tangible movable financial leasing services shall be in a factoring manner. The creditor's rights of the unpaid rent receivable under the finance lease contract shall be transferred to the financial institution such as the bank, and the financial lease relationship between the leaser and the lessee shall not be changed. The value-added tax shall continue to be paid in accordance with the current regulations, and the invoice shall be issued to the lessee. It is stipulated that the seller sells goods or services, and the seller pays the value-added tax. The financial services provided by the factoring company shall pay the difference between the recovered funds and the advance funds in accordance with the “loan servicesâ€.

The fund settlement income obtained by the third-party payment institution shall be subject to VAT in accordance with the “direct fee financial serviceâ€.

Silicone Protector

Made of Soft high-temperature-resistant Silicone (Adhesive Except), Offer 5x cushion, softer and thicker than normal PVC corner protectors. Unlike the foam material, it can not be tore easily by babies and children, but also provide with flexible proofing guard for baby safety.

Our main business is customization Silicone Phone Case,Silicone Rubber Sealing Ring Gaskets Grommets Accessories, Silicone Bracelets, Silicone Watchband, Silicone Keychains , Silicone Kitchenware. Silicone Spoon ,Silicone Stopper, Silicone Placemat Silicone Scrubber,Silicone Baby Products, Silicone Backpack ,Silicone Pet Supplies If you are interested, please consult

YDS Product categories of Silicone For Baby, we are specialized manufacturers from China, Silicone Baby Spoon, Silicone Baby Bibs Silicone Teething Toys,Silicone Plate & Placemat,Silicone Pacifier Holder,Silicone Pacifier & Nipple, Silicone Bowl wholesale high-quality products of Silicone Baby Products Our Factory Advantages:

1.Mold workshop and 2D and 3D engineer department

2.Solid siliccone compression machine and liquid silicone injection machine

3.Disney and Sedex 4P audit factory

4.ISO 9001,IATF16949,Raw material of FDA LFGB MSDS Certificates

. Look forward to your cooperation!

2.Solid siliccone compression machine and liquid silicone injection machine

3.Disney and Sedex 4P audit factory

4.ISO 9001,IATF16949,Raw material of FDA LFGB MSDS Certificates

. Look forward to your cooperation!

Silicone Protector,Baby Locks For Cabinets And Drawers,Locks With 3M Adhesive Pads,Baby Safety Locks

Shenzhen Yindingsheng Technology Co., Ltd , https://www.dgoemsiliconeyds.com