According to the number of monthly independent devices in the iResearch APP Index, the top 55 payment apps in July are as follows (since some payment companies divide their products into wealth management, the following rankings are for reference only):

In July 2017, the basic categories of payment app rankings were released, and Alipay, Wing Payment, Wallet, etc. continued to grow in the number of monthly employees. It is worth noting that UnionPay wallets and Jingdong wallets have actually fallen.

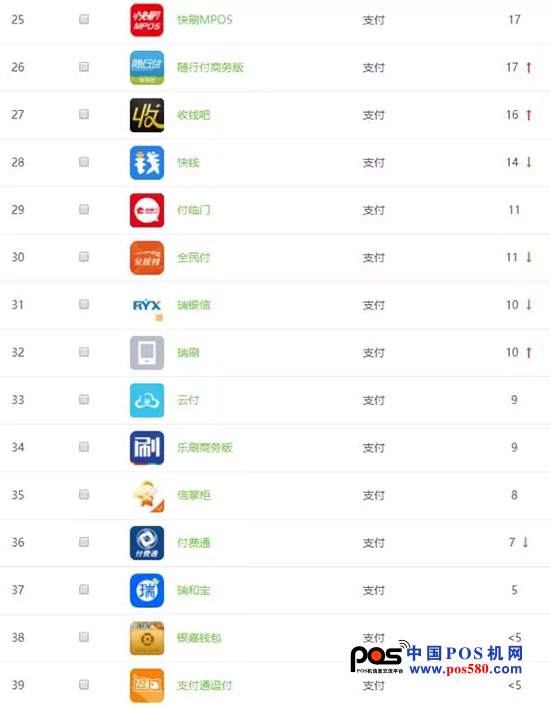

In addition, many of our familiar hand brush products are still very eye-catching. Such as Lakara, PayPal QPOS, Money Box, PayPal, UBS, accompanying payment, music brush, etc. are all on the list. It is also worth noting that in the July list, there were more Tongfu, Fulinmen, Ruihebao, etc., and the rankings were quite high.

The real-time merchant-based aggregation payment brand money party, collecting money, etc. once again on the list, the number of monthly users is amazing, but at the same time there are credit card, flower card set-up as the user base, with alleged pyramid schemes for development The individual brands of the means were also ranked in the top 40, which caused the market to worry about the compliance and regulatory requirements of the aggregation payment brand.

I don't know when it started, the QR code grows like mushrooms all over the place. Whether it is the uncle who sells sweet potatoes or the aunt who sells cool skin, I put a QR code on my mobile booth. Two-dimensional code payment is like a whirlwind that sweeps across China's streets.

With the strong user advantage, Internet payment companies represented by Alipay and WeChat have promoted electronic payment from large merchants to all aspects of our lives. An era of mobile payment has arrived.

Aggregate payment, came into being

Under the spring of mobile payment, all major organizations have started their own mobile payment journey. From banks, UnionPay, Alipay, WeChat, to Jingdong and Baidu, various organizations have launched their own mobile payment products. The clean merchant checkout is occupied by one QR code after another.

However, the problem arises: in front of many QR codes, the consumer does not know which one to sweep; the merchant cashier does not know which platform received the money, and the checkout at night is not a small one here, or one more there. The pen is overwhelming.

Too many payment methods have become a pain point for many merchants and consumers. People can't help but think of it. As early as the 1990s, due to the large number of acquiring banks, the merchants' cash registers were piled up with various POS machines. The problem of one cabinet and multiple machines became the most difficult problem for merchants. The emergence of China UnionPay, the realization of networking and universal, has finally ended the era of merchants with multiple cabinets. Now the problem reappears, although there is not a huge number of pos machines, but the complicated QR code is as annoying as the POS machine of the year.

In this context, in order to solve the merchant's everywhere two-dimensional code, consumers do not know which pain point to sweep, a thing called "Payments Gateway" in the United States was introduced to China, it is now we Said aggregate payment.

What is aggregate payment?

As the name implies, it is a payment interface that integrates multiple Internet payment methods. It uses the payment channels of banks, non-bank payment institutions and transfer clearing organizations to realize the checkout at the merchants through the integration of their own technologies and services. The various QR codes are grouped together to provide a unified platform and back-end management system for merchants. Only one construction can be used to uniformly connect multiple payment methods to merchants, and provide unified reconciliation and Money management provides consumers with a convenient payment experience. Regardless of the payment tool, it is good to scan a code and provide merchants with fast cashier management. Therefore, the emergence of aggregate payment has been widely welcomed by consumers and merchants.

Aggregation payments were introduced around 2015 and have shown a full-blown trend in 2016, and now there are two main models.

The first is the platform rental model. This model is also known as the SaaS model. This model is characterized by a platform built by specialized vendors to provide aggregation of multiple payment methods by providing payment software for merchants, and aggregate payment vendors charge by providing platform software. The merchant is charged a fee based on the API (data interface) call volume.

The second is the traffic split mode. This model is also known as the payment agent model. This model provides a payment platform for merchants by providing a unified payment interface for payment institutions, and provides a payment platform system for merchants, but has nothing to do with the flow of funds. .

Aggregate chaos

Like almost all innovative financial technologies, aggregate payment has developed rapidly, but market standards and norms are far from keeping pace with industrial development. Therefore, the rapid development of the market will inevitably bring many problems. The main issues are concentrated in the following areas.

First, the risk of “two clears†continues to escalate.

What is "two clear"? The so-called "two clears" is a proper term for the payment industry. It refers to the units or individuals that have not obtained the permission of the People's Bank of China to pay for business. With the support of licensed payment institutions, they borrow the channels of licensees to actually engage in payment services and funds. A model of clearing business. In recent years, in the context of the rapid development of the payment market, there are a large number of institutions in the market. Although there are no payment licenses, they are doing payment. As a result, a large number of merchants are not safely secured, and the platform is running away. The occurrence of such events.

Aggregate payment, as the so-called fourth party payment other than traditional third-party payment, is theoretically only an intermediary for information services. All capital flow, liquidation, and risk control are handled by licensed payment agencies, but some There is still a phenomenon in the organization to play the "two clear" edge ball, which has caused the risk of the entire industry. Even some organizations still have the phenomenon of depositing customer funds, which brings serious hidden dangers.

The second is the retention of sensitive information.

In the process of QR code scanning, the user's user ID, user account, transaction flow, and even the user's mobile phone number can be obtained by the service organization of the aggregate payment, then these sensitive information becomes a huge hidden danger. . In the past, many licensed payment institutions have experienced a large number of user information disclosure incidents. As an emerging participant in the market, the aggregation payment organization has weaker information storage and storage capabilities. The presence of such sensitive information in the aggregation payment institution may bring huge Risk hazard.

The third is the problem of bad money driving out good money.

Aggregate payment is different from any of the traditional “four-party model†of the payment industry. The income source of the aggregation payment company is only one service fee. In the context of the transfer settlement fee is very low, it wants to rely on aggregation payment. The service to pay is actually very difficult. However, Chinese merchants, especially small and medium-sized micro-businesses, which are prevalent in aggregate payment, are a kind of extremely price-sensitive people. They are less concerned with the security of funds. Often, which service fee is low, which is too low. The price has caused the problem of bad money in the aggregate payment market to drive out good money. A large number of low-quality service providers are flooding the market. The result of vicious price competition is that the market is more chaotic.

In response to market chaos, the People’s Bank of China’s Payments Department issued the “Notice of the People’s Bank of China’s Payment and Settlement Department on the Implementation of the Cleanup and Remediation of Non-Regular Aggregation Payment Services†and the “People’s Bank of China’s The Guiding Opinions on the Development of the Service Market directly regulates the development of the aggregate payment market from the official point of view. On the basis of positioning the aggregate payment as the “acquisition outsourcing institutionâ€, the regulatory department has drawn three red lines: no core business can be handled. Merchant funds may not be deposited, and sensitive information may not be retained. This marks the country's comprehensive regulation of the aggregate payment market.

Aggregate payment, the tuyere has come

From the development trend of the payment industry, the trend of the industry from one cabinet to multiple machines (one cabinet and multiple yards) to one cabinet and one machine (one cabinet and one yard) is a general trend. With the national supervision and regulation on the whole aspect of the industry The effective intervention of the regulatory layer ended the cycle of the aggregation payment industry bound by the "Grechen's Law", ending the barbaric growth era of aggregate payment, and the development of aggregate payment in the future will usher in a big opportunity for compliance development.

Aggregate payment will develop in the future in a more compliant, healthier and more innovative direction. The main development trends may have the following aspects.

One is multi-scenario aggregation.

With the popularization of mobile smart payment methods such as two-dimensional code and NFC near-field, mobile payment will gradually advance from the shopping field to the diversified field. In the future, whether it is water and electricity coal payment in the public payment field, cable TV payment, or public transportation, Road parking and so on are potential markets for aggregate payments. From the perspective of development, the future aggregation payment is definitely not just a simple scene aggregation of the QR code scene. With the rise of smart terminals such as smart cloud POS, two-dimensional code, NFC near field, IC card swing and other payment methods. Both will be integrated into the broad category of aggregate payments.

The second is multi-agency connectivity.

At present, the main development area of ​​aggregate payment is still the aggregation of two-dimensional code payment, and the aggregation institutions are a few of Alipay, WeChat payment, Jingdong payment, and bank payment. In the future, with the rapid development of aggregation payment, the integrated payment service of integrating bank card receipt, Alipay, WeChat payment, game card, mobile phone recharge card, bus card and other prepaid cards will appear. Multi-institutional multi-connected will have May become a trend of development. With clear market rules, industry leaders such as banks, UnionPay, and non-bank payment institutions are likely to deploy aggregate payment markets, and then guide the market to develop in the direction of diversified scenarios to achieve true diversified payment union.

The third is more financial consolidation.

Payment is the entry point for all financial scenarios. As an entry form, aggregate payments are more likely to be an effective channel for multi-financial integration. In the future, aggregate payment will make it possible to achieve a variety of payment methods, such as account-to-account, real-time reconciliation, and qualified institutions will no longer limit the business to traditional payment services, merchants, water, loans, consumer financing, financial management, Diversified financial services represented by member financial services, etc., will likely emerge, resulting in a diversified competitive advantage for aggregating payment institutions.

The fourth is multi-market penetration.

The current mobile payment is mainly concentrated in the first- and second-tier central cities, and there is a fierce competition in the Red Sea between various institutions. However, in the vast secondary cities, county markets and rural markets, mobile payment is still in its infancy, with a single payment product type and extremely scarce payment services. Simple POS machines or software collection and payment are difficult to meet the growing needs of merchants. The sinking trend of aggregate payment has been formed. Attacking the secondary market and the following markets through the low-cost advantage of aggregate payment will become a possibility for the aggregation payment to open up the blue ocean of the industry.

Aggregate payment has come to the fore, and there will be greater development opportunities after compliance development. And now that the moment of history happens, we are on the scene.

Women'S Backpacks,Mini Backpack With Studs,Leather Backpack For Women,Small Backpack For Women

GUANGZHOU KOEDS LEATHER LIMITED , https://www.kodes-bag.com